Nick's Pick: Aritzia

- willnickerson87

- Jun 21, 2023

- 4 min read

To the dismay of some (and pleasure of most!), Ticker Talking has been rather quiet as of late. However, that all changes today! Maybe not better than ever, but we’re back…and with a new strategy of increasing female readership, beginning with this particular article about Canadian-based retailer (and fan-favourite among the ladies), Aritzia (Ticker: ATZ.TO).

Founded in Vancouver in 1984, Aritzia produces quality, fashionable women’s apparel that operates between the fast-fashion and designer categories—namely the mid-luxury market. Mid-luxury retailers like Aritzia distinguish themselves from fast-fashion companies with higher quality materials and a focus on various elements of ESG like sustainability and human rights (which are become increasingly important to ATZ’s target market of Millenials/Gen Z). A recent McKinsey survey showed that almost all consumers concerned about sustainability earn an income above average and are willing to pay at least 15% more these items – clearly mid-luxury companies like Aritzia stand to benefit from these ESG-related consumer trends. See Exhibit A for ATZ’s Morningstar ESG rating.

Exhibit A

While mid-luxury is not as well-protected as the designer/luxury segment, it is still fairly durable against macroeconomic factors like inflation, rising interest rates, and slowing consumer demand. On earnings call earlier this year, CEO Jennifer was quoted saying, “what we're seeing is, a tremendous amount of consistency between who's shopping with us, what they're buying, their average basket size have not changed, the average selling price has not changed, the number of units has not changed.” Despite many calls for an economic slowdown, so far what we’ve seen is a resilient consumer. However, even if the much-anticipated recession does indeed materialize, having loyal, higher-income customers (whose spending habits are much less correlated with the economic cycle) means Aritzia should have a much easier time than most fashion retailers in weathering the storm.

One of Artizia’s advantages is its variety of clothing and accessories, evidenced by their exclusive brands such as Aritzia, Wilfred, and Babaton, which enable to company to cater to wider range of ages, lifestyles, etc.. It’s also worth noting that Aritzia made its foray into menswear with its acquisition of premium athletic brand Reigning Champ in 2021 (ATZ is projecting revenue of $75M in FY27…currently $25M), giving the former access to a new segment of the market.

Aritzia’s vertical integration is one of the main ways they differentiate themselves from competitors; they oversee the design, sourcing, and retail phases of their operations. Maintaining control over these functions enables ATZ to improve production and quality control and cut down manufacturing costs, but arguably the biggest benefit of keeping the design team in-house is that it allow the company to quickly react to new fashion trends.

While Aritzia has enjoyed considerable topline growth relative to its competitors over the past couple of years (See Exhibit B), I believe that continued US expansion and further investment into the e-commerce business will extend the company’s successful run in the retail fashion sector.

Exhibit B

Aritzia’s US boutiques are expected to generate $1 billion in sales in FY23—given that revenue in the US clothing market amounts to $345 billion, ATZ’s current share is about 0.3%. The company has plans to grow their US presence significantly, doubling US boutiques by 2027 (from 46 to 92) and ultimately overtaking total Canadian stores (See Exhibit C for current North American boutique locations).

Exhibit C

I think that an increased focus on their US business should fuel ATZ’s growth through the rest of the decade; US stores already account for 50% of sales, and the graphic above shows the abundance of opportunities for untapped market expansion. Management has expressed its goal to open in 18 new US markets by FY27.

E-commerce success, the other key to the company’s growth, goes hand-in-hand with store expansion; historically Aritizia’s online business has seen an average boost of 80% when a boutique opens in a new market. Their e-commerce channel currently represents about 35% of sales, and the company expects that figure to grow to 45% in FY27 (See Exhibit D).

Exhibit D

Aritzia has invested heavily in their e-commerce platform, most recently announcing the establishment of e-commerce 2.0, which essentially uses customers’ individual style and preferences to make personalized suggestions. Furthermore, the company has done an excellent job prioritizing the shopping experience by integrating the sales channels—customers can purchase the product online and then get it shipped to a store for pickup, or they can even ship clothes to the store to try on before committing. Consumers value flexibility and convenience even more nowadays, and Aritzia’s e-commerce platform certainly satisfies those criteria.

Now let’s take a look at the stock, which took somewhat of a nosedive after they reported earnings at the end of the last quarter, dropping 20%+. Despite beating top and bottom line estimates, investors were spooked by the sound of gross margin compression (going from 40.4% a year prior to 38.0%). Management issued guidance along the same lines—going forward they expect a 2% decrease in gross margins and a 1.5% increase in SG&A.

Personally, I’m not as concerned as the market – sticky inflation will likely put pressure on margins for the next few quarters, but I see this as a short-term/temporary issue. The forward-looking guidance wasn’t all bad either; ATZ expects revenue for the next quarter to come in 10-13% higher than last year.

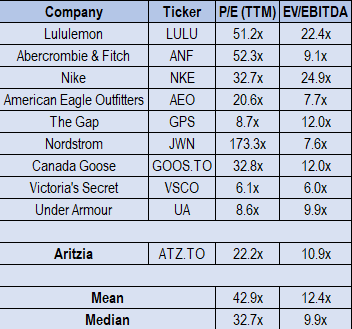

Looking at valuation, compared to peers Aritzia appears to be undervalued (See Exhibit E), especially when you consider that it’s likely to grow faster than most of the names on that list over the next 5-10 years (just look at the YoY growth numbers in Exhibit F).

Exhibit E

Exhibit F

In closing, ATZ shares look very attractive after the recent drop in price. The company is certainly facing some challenges in the near-term relating to the cost of their inputs (e.g. cotton) amid an inflationary period, but we’re long-term investors focused on Aritzia’s plans for the rest of the decade, and in my opinion the investment thesis is still solid. The company is committed to investing in their long-term growth through boutique expansions in the US as well as well as their focus on digital innovation and integrating their sales channels. So next time you’re buying a little Babaton, pick up a few shares to go with it!

Comments