Nick's Pick of the Week: VISA

- willnickerson87

- Jul 19, 2022

- 4 min read

Updated: Sep 18, 2022

I’m very excited to launch a new series here on Ticker Talking (which I’ve decided to name Nick’s Picks), where I (Will Nickerson) will pick (get it now!?) a stock every second week and make the case for why you should consider it for your portfolio. Were there better titles I could’ve chosen? Yes, probably quite a lot of them in fact…but we’re sticking with it!!

As the possibility of a recession looms, if you haven’t already I encourage you to form your buy lists to capitalize on the opportunities that this bear market presents—hopefully this new segment will help you with that. So without any further ado, Ticker Talking’s inaugural stock-of-the-week is Visa (Ticker: V). I think it’s safe to assume that almost all of you have heard of the payment technology giant before. The intention of this article, though, is to focus on Visa’s stock as well as the credit services industry at large, which you may not have as much knowledge about.

Famed investor Warren Buffett said in a 1995 letter to shareholders that in business, he looks for “economic castles protected by unbreachable moats.” Of course, Warren isn’t speaking literally about moats and medieval castles, but instead figuratively about how he searches for companies that have established themselves as industry leaders in markets with high barriers to entry. As a result, from a competitive standpoint, much like a Queen perched up in a moat-protected castle, these companies are next to untouchable.

While at the time of the comment, Buffett was alluding to Geico and how it has fortified itself within the insurance sector, I think Buffett would agree that his analogy very much applies to Visa and its position in the credit services industry (it's worth noting that he held for Visa stock for over 10 years before selling earlier this year).

This is because of the scale of Visa’s network; operating in over 200 countries, more than 100 million vendors use the company’s services. Furthermore, there are currently about 3.8 billion Visa cards in use, and In 2021 transactions going through Visa’s system totalled over $13 trillion. For context, Mastercard (Ticker: MA), who has developed an exceptional payment network of their own, has 2.5 billion active cards and saw a total volume of $7.7 trillion through its network in 2021. It would be next to impossible for a new company to come along and set up a payment network that could rival Visa’s in size or volume—in terms of our analogy this speaks to the business’s incredible moat.

The moat starts to look even larger when you realize that Visa establishes the rules for the world’s largest payments network (possessing considerable pricing power). Visa gets a cut of every transaction that goes through its network, and say if they wanted to increase their fees they would be able to do so without losing a substantial amount of customers as most vendors have to accept Visa due to the sheer number of cardholders worldwide. While the moat is very much applicable to the business, Visa’s network and business model can be likened to a tollbooth setting the price of entry for vehicles to a major highway.

Exhibit A - Visa network facilitating transfer of funds in transaction between consumer and merchant

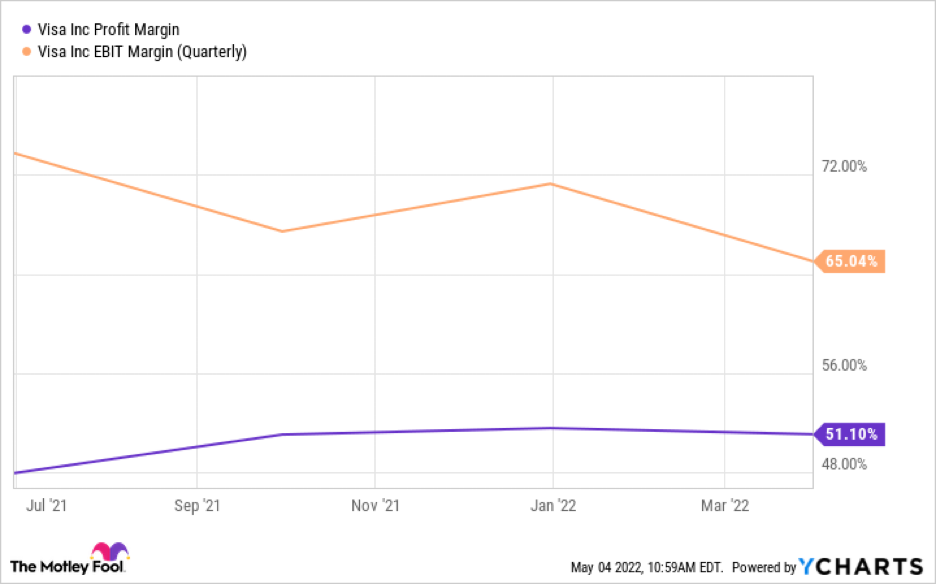

Still not impressed? Let’s take a look at some of the financials. Visa’s profit margin as of May 2022 was a staggering 51%, meaning for every dollar of revenue Visa is pocketing about $0.51. Two of Visa's biggest competitors, MasterCard and American Express, lagged behind with their 2021 profit margins coming in at 46% and 18%, respectively.

Exhibit B - Visa’s Margins

You may be wondering how Visa could be impacted by the inflationary environment we are currently seeing. The answer is it really shouldn’t be affected—not much anyway—as most costs associated with its payments network are fixed and since their fees are a % of transaction cost (variable), if prices of goods and services increase, so too should Visa’s cut, or revenue per transaction. However, inflation and interest rate hikes do present a greater risk of credit cardholders defaulting on their payments, so it will be interesting to see how Visa handles that potential threat. Payments companies like Visa are also likely to face currency headwinds as the US dollar has strengthened against other global currencies in recent months (mainly due to rising interest rates making the idea of holding dollar deposits in interest-bearing accounts in the US more attractive). While a strong dollar is great for Americans looking to travel and spend money abroad, it isn't ideal for Visa and other US companies that rely on revenue from overseas (54% of Visa's revenue came from outside the US in 2021) as they'll see their earnings drop when the currency conversions are factored in. Additionally, a recession could be detrimental to the business in the sense that it might be accompanied by reduced consumer spending (a driver of Visa’s revenue), but the company made it through 2020 (which had a very brief recession) while seeing just a slight dip in revenue and an increase in its share price.

Finally, past performance is no guarantee of future results, right? That is certainly true, but I think Visa’s stellar history gives a good indication of its long-term performance going forward. The world has been moving away from cash; however, what’s fascinating is that about 50% of global transactions are still done with cash! This shows that the business clearly still has a large runway for growth as it adds new countries and merchants to its network, which should only encourage people like you and me to invest in the payments technology giant and its unbreachable moat!

Comments