Starting the Year off REIT (with Allied Properties and Prologis)

- willnickerson87

- Jan 4, 2023

- 6 min read

Updated: Jan 4, 2023

Once again, it’s been a little while since you’ve heard from me…did you miss me?? Actually you know what, don’t answer that! I’m telling myself that you’ve all been pining for another article!

Happy New Year, by the way! As I reflect on last year, I must say that I’ve really enjoyed doing these blog posts over the last 8 months or so, and I very much appreciate each and every one of you, for taking the time out of your busy lives to listen to what I have to say.

Now, without any further ado, let’s get into the first article of 2023—consider it my belated Christmas gift to you! Although calling this a full-on gift might be a bit bold…this could be more of a stocking stuffer…but ultimately I’ll let you make that determination! This holiday edition of Ticker Talking is centred around real estate, and the inspiration for this topic came from one of Ticker Talking’s most distinguished readers (and investors!), who suggested I look into a particular REIT (Real Estate Investment Trust). I figured it would make a great post, especially considering that my real estate coverage has been minimal so far.

There are several advantages of investing in real estate, one being the tangibility factor - your investment is backed by a physical asset that you can see, feel, and utilize. Thus, oftentimes it experiences less volatility than an asset like stocks, where (although still rare) you are more likely to see the value of your investment being reduced to $0 (take Enron, for example, which went from Wall Street darling to bankrupt quicker than you can say Jack Robinson). It should be noted, though, that while equities may be a riskier proposition, the stock market has delivered historical returns greater than those of real estate.

Real assets historically have outperformed stocks and bonds in inflationary environments. This is because the economic drivers of real assets tend to be closely related to inflationary trends, thereby yielding immense returns during periods where inflation is high (and relatively poor results when inflation is below expectations). Specifically, one of the driver’s of the recent inflation has been the release of pent-up consumer demand - this has contributed to the success of real assets such as commodities, natural resource equities, certain real estate sectors, and infrastructure, which were notable under-performing industries in the early stages of the pandemic.

In terms of real estate’s ties to inflation, property values typically rise with the general price environment as labour, land, and materials costs increase. Additionally, some leases (usually commercial) may have inflation-related rent escalators, but in most cases sectors with shorter-term lease durations are best positioned to quickly capitalize on inflationary periods.

Despite the fact that several real estate asset classes are well-suited to fend off many inflation-induced challenges, real estate didn’t exactly have a stellar 2022, evidenced by the performance of the Dow Jones U.S. Real Estate Index (this tracks performance of REITS and other companies that invest directly/indirectly in real estate), which on a total return basis was down roughly 25% for the year (See Exhibit A).

Exhibit A

The primary cause of the REIT sell-off is investors’ jitters over the rising interest rates, which has obviously made debt financing more expensive (applicable to new loans of course but also costlier for REITs looking to incrementally refinance their maturing debt).

However, as value investors, we shouldn’t turn a blind eye to market weakness and the opportunity it often presents. The REIT that I was tipped off about was Allied Properties (Ticker: AP-UN.TO), a company headquartered in Toronto that owns, manages, and develops urban workspace in Canada’s major cities as well as network-dense urban centres in Toronto that “form Canada’s hub for global connectivity.”

Allied was a fan-favourite among investors leading up to the pandemic, with shares reaching an all-time high of about $60 in February 2020. However, much like the overall real estate market, the stock has been hit hard this past year (down close to 45%); the major factors being the work-from-trend and its impact on office demand, and higher interest rates, as I mentioned. It was reported at the end of November that Allied Properties is considering selling its downtown Toronto data-centre portfolio (responsible for 16% of Allied’s net operating income), which the company estimates is worth around $1.3 billion. The business would use the proceeds to pay down its debt in an effort to adapt to the new era of hybrid work and high interest rates (Allied’s net debt is currently about 10x EBITDA, as opposed to 6.7x EBITDA pre-pandemic).

The most appealing aspect of Allied Properties’ stock is its dividend; the forward yield is currently about 7%. This is certainly on the higher end for the industry (higher than its historical rate mainly due to the falling share price this year) - the average dividend for REITs is about 5%. Therefore, even if the stock price doesn’t appreciate whatsoever next year, you’ve already made a decent return of 7% (especially when you consider the expected market volatility in 2023). It’s very unlikely for the Allied’s dividend yield to remain that high—in the long-term I expect it to return to about 4% (around its historical average over the last decade).

I must say that I’m hesitant about investing in any type of office real estate these days considering the permanence of remote work and the resulting vacancy rates of office space in major cores like Toronto, New York, etc. The U.S. national office vacancy rate is currently 17.1%—it’s highest mark since 1993. Allied’s pre-Covid occupancy rate was about 95%, but it has since slipped to about 90% (according to September 2022 quarterly report), which is still respectable (when compared to the office real estate sector) but shows that it is by no means absolutely immune to demand fluctuations.

Despite the apparent waning office demand, some segments of the market are doing better than others. Specifically, the high-end spaces (i.e. modern offices in great locations with plenty of amenities like restaurants, great views, etc.) are performing relatively well, with demand remaining strong. You’re seeing companies trading up in office space—this flight to quality can seemingly be attributed to retaining employees (and trying to get them to come back into the office) as well as drawing in new talent. This trend of Grade A real estate being well-equipped to weather this demand storm makes me more of a believer in Allied Properties; their Class I workspaces in amenity-rich downtown neighbourhoods are very modern and innovative, evidenced by the open-plan with abundant natural light and fresh air. Corporations like Google, which are driven by continuous employee innovation and creativity, are major proponents of these workspaces as they find that it provides the optimal atmosphere in terms of employee engagement and productivity.

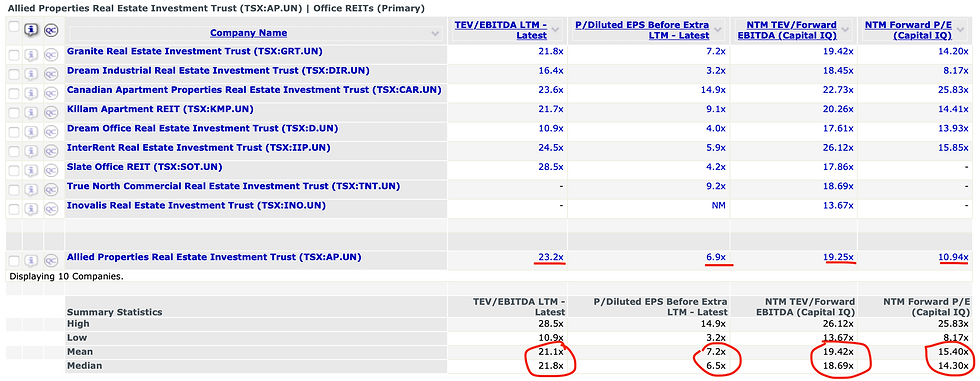

Allied’s stock looks quite cheap at the moment if you’re looking at its historical performance—the stock price hasn’t been this low since about 10 years ago (when the Adjusted Funds From Operations per share was around 35% lower). Furthermore, it’s currently trading at about 50% of the company’s NAV (Net Asset Value), where the market has traditionally valued the stock 10-20% above the NAV. However, when compared to REIT peers (not only in the office sector) Allied’s valuation becomes less appealing simply because across real estate asset classes almost everything has become cheaper, which is clear from the trading multiples of competitors seen in Exhibit B.

Although I think if you invest your money in Allied Properties’ stock at the current price, you will make a solid return (both from price appreciation and dividends), personally I would gravitate to real estate asset classes that are poised for more rapid growth. In my opinion, that starts with industrial and logistics real estate, and in terms of a specific REIT look no further than Prologis (Ticker: PLD). Prologis is a major supply chain logistics player; the company owns and operates about 985 million square feet of shipping and order fulfillment facilities. PLD shareholders have fared well over the last couple decades, netting themselves an annualized return of 10.8% (with dividends reinvested) dating back to 1998. Much of this success can be attributed to the boom in e-commerce and shipping from tenants such as Amazon and Fedex. I believe that the logistics giant will continue to flourish as e-commerce and online shopping keeps growing—the fact of the matter is that companies need more space to store (and deliver) their products, and Prologis is set to capitalize on the increase in demand as a dominant player with presences in important global markets.

From a valuation standpoint, just like with many companies in 2021, PLD shares went on a big run into over-valuation territory; however, they’ve since corrected and appear to be around fair value (and in line with the fundamentals). Relative to comparable companies, Prologis’ forward P/E indicates that the company’s shares are reasonably priced (See Exhibit C).

Exhibit C

To conclude, I think that real estate will have a better year in 2023—for starters we should (fingers crossed) be nearing the end of the interest rate hiking cycle, and valuations across the board are very attractive at their current price points. I like both of these companies that I’ve outlined; however, at the moment I’m more inclined to invest in Prologis given that I believe logistics real state has more upside/growth potential in the context of today’s world.

Comments